Author:

Sophie Jamieson

Investment Manager,

Saltus Asset Management Team

Reviewed by: David Cooke, Co-Chief Investment Officer , Saltus Asset Management Team

As we entered 2026, the backdrop for investors looked broadly supportive. Inflation had moderated from its post-pandemic highs, interest rates appeared close to their peak, and the global economy continued to demonstrate surprising resilience, helped by a fresh wave of corporate investment in artificial intelligence (AI) infrastructure.

For a time, this looked like the continuation of a comfortable trend, with growing confidence that central banks could guide inflation back to target without triggering a slowdown.

Then came March. The conflict in the Middle East triggered a significant energy shock. The closure of the Strait of Hormuz, causing disruption to the global supply of oil and other critical commodities, pushed prices higher forcing a rapid repricing across financial markets.[1] Equities fell, bond yields rose and investors were left to reassess the consequences of a prolonged conflict.

Yet, as so often during periods of geopolitical stress, markets ultimately proved willing to see past the immediate shock. As the second quarter progressed, investors increasingly concluded the conflict would be contained and that the spike in oil prices would prove temporary.[2] Following the announcement of a ceasefire framework, that assessment appeared broadly correct. Equity markets recovered strongly and, by the end of June, many risk assets had regained their losses and moved on to fresh highs, despite the longer term resolution of tensions in the region remaining uncertain.

Inflation strikes back

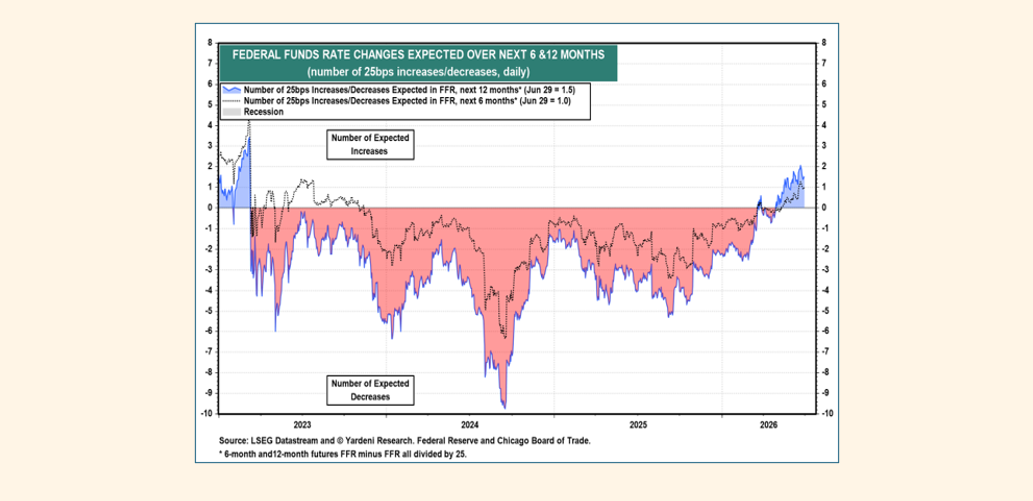

For much of the last three years, investors had operated within a relatively familiar framework: inflation was expected to fall steadily, central banks would eventually cut interest rates, and declining bond yields would provide a supportive backdrop for both equities and bonds. As 2026 has progressed, that assumption has begun to be challenged.

In many ways, this marks the first meaningful change in momentum investors have faced since inflation peaked in 2023. For several years, markets were largely debating when interest rates would begin to fall. Today, the conversation has shifted towards whether they may need to rise further.

Importantly, inflationary pressures were beginning to build even before the conflict erupted. Strong economic activity, tight labour markets and sustained investment spending had already raised questions about how quickly inflation would fall back to target. The energy shock simply accelerated a trend that was already becoming visible in the economic data.

Evidence of that shift is already emerging. Inflation has moved higher again across several major economies and central banks have responded accordingly. The US Federal Reserve has paused its anticipated easing cycle[3], whilst the European Central Bank has raised interest rates for the first time since 2023[4].

This matters because interest rates influence virtually every asset class. They affect borrowing costs, company valuations and the price investors are willing to pay for future growth. The impact is rarely immediate, but over time higher rates exert a gravitational pull on asset prices.

Do you need help managing your investments?

Our team can recommend an investment strategy to meet your financial objectives and give you peace of mind that your investments are in good hands. Get in touch to discuss how we can help you.

The AI trade: opportunity or concentration?

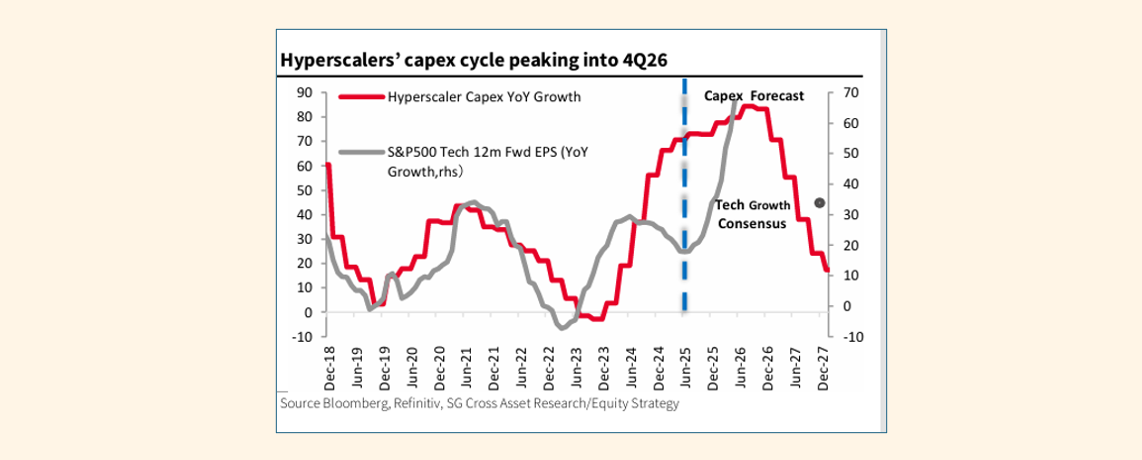

The buildout of AI infrastructure has been one of the defining investment themes of recent years and remains a genuine engine of economic growth.[5] Huge sums continue to be invested in semiconductors, data centres and computing capacity, helping support both corporate earnings and broader economic activity.

Indeed, a significant proportion of the economic resilience seen this year can be traced back to the enormous capital spending programme underway across the technology sector. At a time when many expected higher interest rates to weigh on growth, AI-related investment has continued to provide a powerful source of demand.

However, much of the market’s recent performance has been driven by a relatively small number of very large technology companies. Whilst many remain exceptional businesses with strong competitive advantages, market leadership has become increasingly concentrated.

At the same time, the debate itself is starting to evolve. The first phase of the AI story was largely about who would invest the most. Today, investors are becoming increasingly focused on whether that investment can generate an attractive return.

The scale of spending remains extraordinary, but signs are emerging that the market is becoming less interested in how much money is being deployed and more interested in what it ultimately delivers. In other words, the conversation is gradually shifting from capital expenditure to profitability.

The next phase is likely to focus on productivity gains, commercial applications and earnings growth. We remain optimistic about the long term opportunity AI presents, but after a period of extraordinary enthusiasm, expectations are now exceptionally high. In such conditions, even good news can struggle to exceed what is already priced into markets.

What diversifies a portfolio now?

At Saltus, diversification has always been a cornerstone of our investment philosophy. The question facing investors today is not whether diversification matters, but which forms of diversification are likely to prove most effective in the environment ahead.

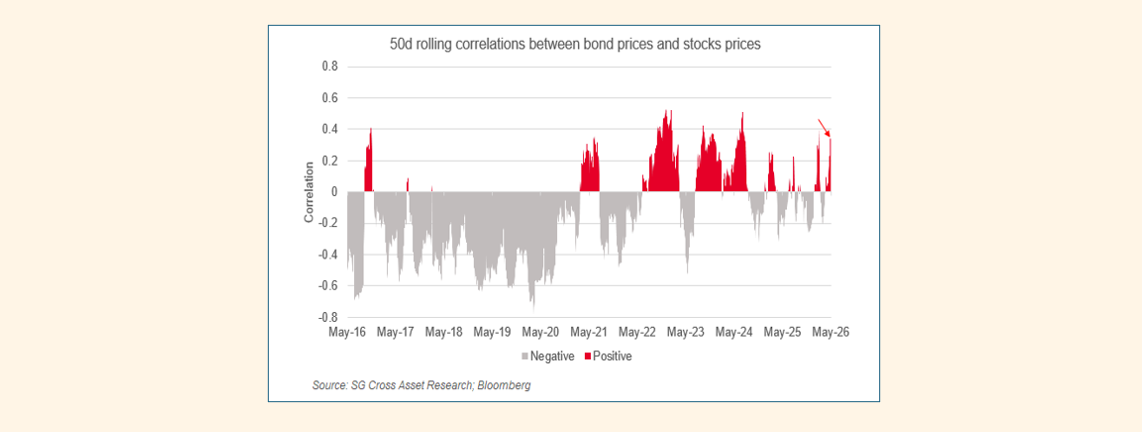

For much of the last two decades, government bonds have provided reliable portfolio ballast. When growth concerns emerged, bond yields typically fell, helping support fixed income returns and offset weakness elsewhere in portfolios.

Periods of higher inflation can challenge that relationship.

If inflation becomes investors’ primary concern, both bonds and equities can come under pressure simultaneously. This does not mean bonds no longer have an important role to play, but it does suggest investors may need to think more broadly about where portfolio resilience comes from.

We believe this reinforces the case for broad diversification across geographies, asset classes and investment styles, alongside the selective use of alternative investments that can behave differently during periods of inflation, volatility or economic stress. A broader mix of assets may prove increasingly valuable as investors navigate the next phase of the cycle.

Final thoughts

As we look towards the second half of 2026, our outlook remains cautiously optimistic.

The foundations of the global economy remain healthy. Corporate balance sheets are generally strong, unemployment remains low by historical standards and innovation continues to support investment and productivity growth.

At the same time, inflation has proved more persistent than many expected, bond yields are moving higher and markets have become increasingly reliant on a narrow group of leaders. The gains delivered during the post-pandemic recovery are unlikely to be repeated indefinitely.

This does not mean we are becoming pessimistic. Rather, we believe markets are entering a more mature phase of the cycle – one in which returns remain available, but are likely to be harder won, and where volatility and reversals may become more frequent.

Gravity may have returned to markets, but that is not necessarily a negative. Markets often deliver their healthiest long term returns when valuations, earnings and economic fundamentals matter again. Whilst the path ahead may be less straightforward than the last three years, we continue to believe that patient investors, supported by diversified portfolios and a disciplined investment process, remain well positioned to navigate the opportunities and challenges that lie ahead.

Article sources

Editorial policy

All authors have considerable industry expertise and specific knowledge on any given topic. All pieces are reviewed by an additional qualified financial specialist to ensure objectivity and accuracy to the best of our ability. All reviewer’s qualifications are from leading industry bodies. Where possible we use primary sources to support our work. These can include white papers, government sources and data, original reports and interviews or articles from other industry experts. We also reference research from other reputable financial planning and investment management firms where appropriate.