Author:

Jordan Gillies

Head of Business Development and Marketing,

Saltus Asset Management Team

Reviewed by: Megan Jenkins, Chartered Financial Planner, Saltus Asset Management Team

If you have come across the term ‘in-specie transfer’ and wondered whether it relates more to zoology than wealth management, you are not alone. The phrase can sound misleading at first glance, yet it describes an important decision point when moving investments from one wealth manager, or financial provider, to another. While both in-specie and cash transfers can be used to move investments to a new provider, they differ vastly in terms of complexity, costs, timelines and administrative demands.

In practice, a cash transfer is typically far simpler and faster than an in-specie transfer. That said, there are circumstances where an in‑specie transfer may be appropriate. Understanding how each works enables you to form clearer expectations around the process and choose the route that best supports your wider financial objectives.

What are in-specie transfers?

An in-specie transfer is the process of moving investments “as they are” from one provider to another without selling them first.[1] Rather than converting your holdings into cash and repurchasing them at the new platform, the assets remain invested throughout the transition. This process can include shares, funds, bonds, or other eligible securities.

Because an in-specie transfer does not sell your assets, it can help preserve market exposure during the transition. It can also reduce the risk of crystallising gains unintentionally, which may be relevant if you hold portfolios outside tax-advantaged wrappers such as ISAs or pensions, where disposals could create a Capital Gains Tax (CGT) liability.[2]

However, in-specie transfers are typically far more complex and slower than cash transfers. Not all investments can be transferred this way and eligibility depends on whether the receiving provider supports the specific fund classes or securities you hold. Some wealth managers use proprietary or non-standard share classes that cannot be moved across, which means those positions may need to be sold and transferred as cash instead. In-specie transfers take significantly longer than a cash transfer and can be more expensive as they require more administrative coordination between providers.

This is why, in practice, most UK transfers do not follow this route. Industry data from Origo, which processes over 80% of UK defined contribution pension transfers (1.5m transfers worth over £66bn in 2024)[3], shows that over 90% of transfers are ‘simple transfers’. [4] These are transfers where the existing provider retains control of the process from start to finish. There are also no structural complexities or potential delays waiting for third party fund managers.[5] By definition then, the majority if not almost all of these will have likely been cash transfers. These simple transfers are typically completed in around 10 working days on average and timelines have been trending downward in recent years.[6], [7]This is in stark contrast to the multiple weeks and, more often quoted, months that an in-specie transfer may take.

In-specie vs cash transfers

Cash transfers typically provide the most frictionless journey for the investor. The time taken to transfer more commonly meets customer expectations and the opportunity for errors can be significantly reduced compared to in-specie. If the assets are held in an ISA or pension and therefore there are no tax implications for selling the assets, there would usually need to be a good reason for a Saltus adviser to suggest anything other than a cash transfer.

One of the main differences between in-specie and cash transfers is time in market. An in-specie transfer keeps your existing investments intact, allowing them to remain fully invested while they move to the new platform. This approach can help preserve market exposure and reduce the risk of crystallising gains in taxable accounts.

However, in practice your money is often not actively managed during this period, because the old provider cannot trade once the transfer begins and the new provider cannot act until assets arrive. While the underlying holdings will continue to rise and fall in line with market movements, no portfolio decisions are usually being made. Given that in-specie transfers can take several months, this may result in an extended period without active oversight or rebalancing.

A cash transfer involves selling your investments with the current provider and transferring the proceeds as cash before reinvesting them on the new platform. This can offer a clean break from legacy holdings and may be preferable if you intend to reshape your portfolio or move into a different investment strategy. While selling down means you are out of the market for a short period, this timeframe is limited and is usually measured in days rather than weeks or months. The associated market risk is generally modest, although it will depend on prevailing conditions and the operational efficiency of both providers. By contrast, an in-specie transfer can leave you with a mixture of old and new holdings for a prolonged period, as some assets may transfer in-specie while others must be sold if they cannot be reregistered. This creates a temporary, unintended “hybrid” portfolio in which a portion of your investments is out of the market anyway, which can be more disruptive than the short, defined break associated with a cash transfer.

It is also important to consider costs, as cash transfers are often free, whereas in-specie transfers can attract fees depending on the provider and the assets involved. For investors with larger portfolios, for example 25 to 30 holdings, these charges can add up quickly and make the in-specie route significantly more expensive overall.

As eligibility, tax considerations and personal objectives differ person to person, a financial adviser can help you understand the implications and choose the approach that best fits your wider financial plan.

Do you need help with your retirement planning?

Our specialists can help you prepare for retirement and provide ongoing advice once retirement has arrived. Get in touch to discuss how we can help you.

In-specie transfers for a General Investment Account

When it comes to General Investment Accounts (GIA), it may be more beneficial to complete an in-specie transfer over a cash transfer if you have significant unrealised gains. This is because disposals in a GIA are treated as chargeable events, so if your holdings have risen in value, selling them simply to move provider could trigger a gain that counts toward your annual CGT allowance of £3,000.[8] Even here though, given how low the CGT annual allowance has become (if gains are high) it may take a very long time to re-structure the portfolio you are transferring by using your annual allowances only. A sale and taxable event can still, at times, be the best option.

Working with a financial adviser can help you manage your annual CGT allowance effectively and determine which transfer method is most appropriate for your circumstances.

In-specie transfer timelines

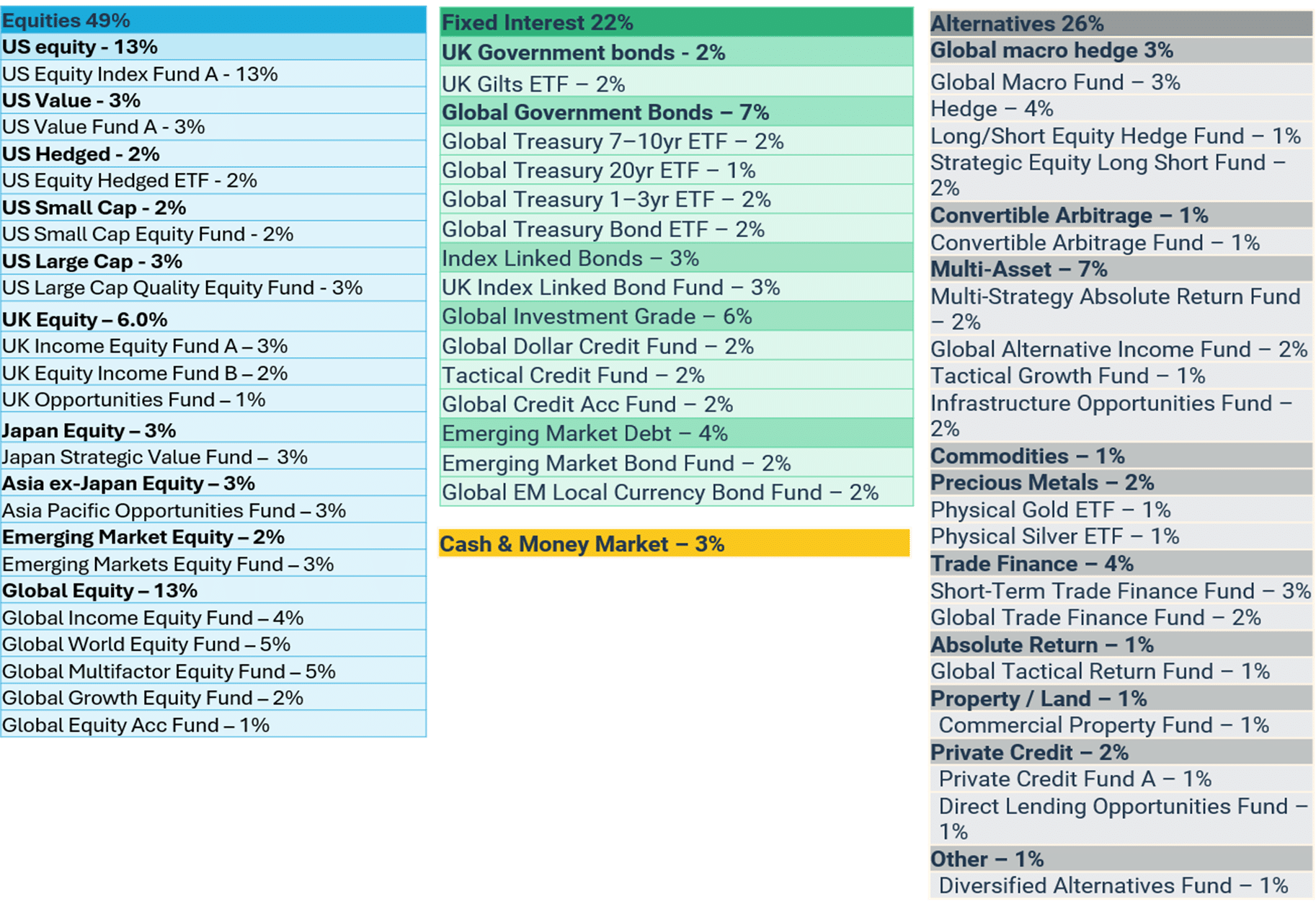

In-specie transfers take significantly longer than cash transfers because every individual holding must be moved separately. An in-specie transfer may take around three to five months, although the timeframe can be shorter or longer depending on various factors including individual circumstances and whether securities have already been set up. This is because a typical diversified portfolio, like the example of our Saltus Multi Asset Class portfolio shown below, could contain dozens of funds across multiple asset classes. Each fund has to be contacted in turn, with instructions processed by different fund houses, custodians and administrators, all working to their own timelines and operational procedures. It’s also worth noting the process for pensions stock transfers typically takes longer than ISAs or GIAs.

Source: Saltus Multi Asset Class portfolio

This creates a chain of separate approvals and checks, and it only takes one fund to be delayed for the overall transfer to slow down. Some holdings may also be in share classes that are not eligible for an in-specie transfer, which introduces extra steps if they need to be converted or sold.

Because so much of the process relies on external parties, the time it takes is not something a financial adviser or wealth manager can control directly. They can coordinate, chase and manage communication, but they cannot influence how quickly each fund provider completes its part of the process. A financial adviser can help set expectations around these timelines and explain which of your holdings are likely to be straightforward and which may take longer to move.

Is an in-specie transfer right for you?

Deciding whether to move investments in-specie or as cash depends on how you want your portfolio to behave during the transition and how each method aligns with your wider financial plan. For most investors, and as industry data shows, a cash transfer is generally the simpler, faster and more predictable option. An in‑specie transfer may still be appropriate if avoiding taxable gains or preserving specific holdings is a priority. A financial adviser can help you weigh these considerations and understand the tax and operational implications before you begin the process.

Article sources

Editorial policy

All authors have considerable industry expertise and specific knowledge on any given topic. All pieces are reviewed by an additional qualified financial specialist to ensure objectivity and accuracy to the best of our ability. All reviewer’s qualifications are from leading industry bodies. Where possible we use primary sources to support our work. These can include white papers, government sources and data, original reports and interviews or articles from other industry experts. We also reference research from other reputable financial planning and investment management firms where appropriate.