Author:

Jamie Havard

Chartered Financial Planner,

Saltus Asset Management Team

Reviewed by: Megan Jenkins, Chartered Financial Planner, Saltus Asset Management Team

Capital Gains Tax; a complex tax that refuses to stay the same, with each government adding its own take on what ‘Simplifying’ looks like [1]

Figure 1, an excerpt from an analysis by the IFS, demonstrating that this isn’t the first acknowledgement of the complexity of Capital Gains Tax. (J.R.King 1985). [2]

Keeping hold of that tradition, the most recent changes came into force on the 6th of April 2024 (and may change again with a new government inbound).

So what are the changes?

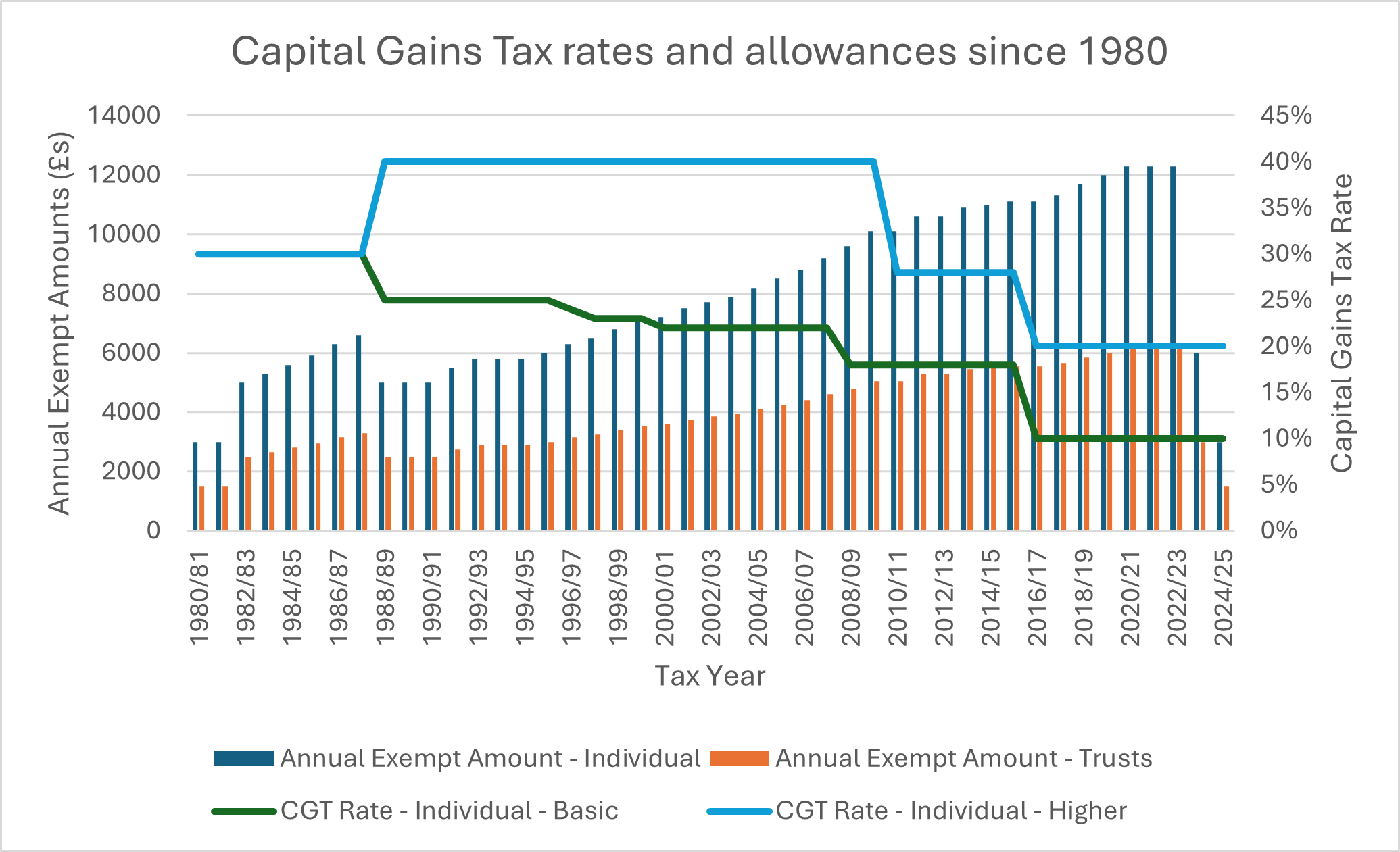

- The higher rate for gains on residential property has reduced from 28% to 24%.

- The Capital Gains Tax allowance [3] has now reached a new low of £3,000 for individuals after trending higher in recent years (reaching the lofty highs of £12,300 in 2020/21 – 2022/23).

A reduction in tax rates is usually well received for fairly obvious reasons (even if this only benefits higher/additional rate property owners), but a reduction in tax allowances is seen more negatively as this applies to all tiers of earners.

By lowering the allowance available the proportion of realised gains that becomes taxable increases. For example, the sale of an asset outside of a tax wrapper (such as funds held in a General Investment Account) has a much higher likelihood of incurring a tax liability now than in previous years, with investors previously not paying capital gains tax now caught by this change.

In previous tax years, the larger allowances available enabled tax planning to happen relatively easily and ad-hoc sales during rebalancing of portfolios wouldn’t move the dial much either. Based on this information, my clients have been quite happy to spread sales over a few tax-years to pay minimal capital gains tax. With the allowances now so small, a portfolio rebalance (where shares are bought and sold to maintain the chosen investment strategy) for large accounts with multiple holdings is more likely to now incur capital gains in excess of the allowance, and the same tax planning to avoid CGT would now take much longer to achieve the same work previously.

For my more ‘tax-led’ clients, the mere thought of paying capital gains tax amounts to heresy.

But is paying CGT really as bad as people think?

Hear me out:

Historically, CGT has been rated at 30%, income tax rates, 18/40%, 18/28%, before settling on todays rates of 18/24%.

We cannot predict the future decisions of the next government, but we can make decisions based on what we know now, and what has happened before.

- Capital Gains Tax is a sign of having made good financial decisions

You have invested wisely, maybe a little too wisely. Your assets have grown and you are going to have to pay some tax to reap your reward, and only on the growth not the capital. It is a clear indication that things have been going in the right direction for your finances. If that doesn’t quite sit, would you rather instead see losses and definitely have no tax liability?

- Dividend allowances are also much smaller, and Savings allowances are relatively smaller following rate rises, meaning more income tax by not tackling built up gains.

Dividend allowances have dropped to £500 for the 2024/25 [6] before tax is charged, and interest rate increases now mean that income tax on savings and bonds are now highly likely. By holding onto an asset that earns these income streams, rather than paying Capital Gains tax at 18% or 24%, income tax is instead being charged at 20/40/45% on interest and 8.75/33.75/39.35% on dividends.

- Potential Inheritance Tax implications

Current legislation has that the base cost of an asset is rebased to the value of the asset on the date of your death. For example, a shareholding of £250,000 with a base cost of £100,000 implies an unrealised gain of £150,000. On death, the shareholdings base cost is revalued to the value on date of death, from £100,000 to £250,000, so now there is no gain thereby removing any potential gains you’d built up in your lifetime [7]. Great news!

However, by not tackling these gains in your lifetime and incurring gains at 18% for basic rate taxpayers or 24% for higher and additional rate taxpayers on only the gains in your lifetime, you’ve instead potentially passed on an Inheritance Tax bill of 40% on the entire holding to your descendants. Not so good news!

For example, Brian holds £300,000 of company shares with a £150,000 unrealised gain. Selling the entire holding to diversify elsewhere or gift away would have incurred at most £36,000 of tax (24% of £150,000). Should Brian have done nothing, there would be no CGT but Brian has an estate in excess of his Nil Rate Bands which means this holding will likely be liable to IHT. This means that his executors will have to pay £120,000 (40% of £300,000) due to inheritance tax.

Sometimes trying to avoid paying tax ends up leading to more being paid (even if you are not necessarily around to see it!).

Do you need help with your retirement planning?

Our specialists can help you prepare for retirement and provide ongoing advice once retirement has arrived. Get in touch to discuss how we can help you.

- Diversification is key

By shutting down the ability to act on an asset because of built up gains, the risk of an asset becoming overweight in a portfolio increases. By not shying away from incurring some tax, you can continue to manage assets with little restriction and maintain a well-balanced diversified portfolio. Tax should not paralyse your investment strategies.

- “The value of investments and the income from them can go down as well as up”.

The investment industry’s favourite disclaimer. It gets plastered all over advertising material to highlight the volatile nature of investing. So when your assets have done well recently, tax should not be a barrier to realising some of these gains. The returns will fluctuate again in future as markets always have done!

- Enjoy the growth

What’s the point in holding an asset if you are unwilling to eventually use it to meet your lifestyle objectives! A potential tax liability should not be the reason to hold back on meeting your objectives whilst you have the health and the inclination to do so.

So it’s not all bad then?

No. It isn’t.

Yes, with 0% allowances as low as they are for CGT, dividends and savings interest, it is much more likely that tax will now be incurred in your day-to-day life, with it becoming a regular occurrence to do so.

But instead we can see this as an opportunity to be proactive with your finances, to get more funds into tax wrappers where possible, to tackle gains at the lowest rates of CGT they have been in 40 years, and most importantly, to reap the reward, take some profit and enjoy the proceeds. You might as well enjoy it!

This article only relates to Capital Gains Tax within England and Northern Ireland. Bandings do differ when discussing Scottish and Welsh taxation bands.

Article sources

Editorial policy

All authors have considerable industry expertise and specific knowledge on any given topic. All pieces are reviewed by an additional qualified financial specialist to ensure objectivity and accuracy to the best of our ability. All reviewer’s qualifications are from leading industry bodies. Where possible we use primary sources to support our work. These can include white papers, government sources and data, original reports and interviews or articles from other industry experts. We also reference research from other reputable financial planning and investment management firms where appropriate.